The New ISSB Standards are Here: What Does this Mean for Companies in Asia?

The Purpose Business applauds the International Sustainability Standards Board’s (ISSB) inaugural standards, International Financial Reporting Standards (IFRS) S1 and S2, which are intended to be the foundation for a comprehensive global baseline of sustainability disclosures. The standards signal an end to the era of the bitter alphabet soup of reporting standards by creating a unified pathway to reporting, with a specific focus on financial materiality. They strive to incorporate industry best practice vis-à-vis existing standards and aim to increase transparency, comparability, and consistency in sustainability disclosure across global capital markets.

The standards have been widely received with enthusiasm, garnering the support of over 40 governments and central banks, including those in Hong Kong and Singapore.

Finally Harmonising Existing Frameworks

The incorporation of frameworks such as the industry-centric Sustainability Accounting Standards Board (SASB) standards — now integrated into the IFRS Foundation — and the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD), was central to the development of the ISSB standards. This is good news for companies that have previously embraced these frameworks, as they’ll be rewarded with a relatively smooth transition to the new requirements. First time reporters may find relief in the inclusion of SASB standards, which allow for a sector specific approach to sustainability challenges, enhancing both transparency and relevance. Whilst the Global Reporting Initiative (GRI) standards will continue to serve as stand-alone guidance and adopt a double materiality approach, addressing the needs of a broad range of stakeholders, GRI and the IFRS Foundation are committed to ensuring complementary and interoperable standards. The application of both sets of standards will efficiently meet the needs of the entire suite of stakeholders as well as provide a holistic approach to identifying sustainability risks and opportunities.

Regulatory Alignment

First movers in Asia include regulators in Hong Kong and Singapore, who are gearing up to adopt the ISSB standards, albeit customised to local contexts. Singapore aims for listed companies to start using ISSB-aligned climate disclosures from reporting year 2025 and unlisted companies with revenues of at least S$1 billion from 2027. Hong Kong is crafting a local ISSB adoption roadmap, considering specific regional nuances. HKEX anticipates updates to their existing ESG reporting based on the ISSB Standards by 1 January 2024, meaning reports issued in 2025 will need to be compliant. Both Hong Kong and Singapore are building in an additional year – beyond ISSB’s suggested buffer of one year – for companies to prepare for disclosing Scope 3 GHG emissions.

ISSB itself doesn’t stipulate external assurance but local regulators may impose such directives. Moves are afoot in Singapore, for example, to mandate such assurance. Companies elsewhere should remain vigilant and anticipate the potential for tightening regulations. Irrespective of regional nuances, it's imperative for companies to establish and maintain robust processes and controls, ensuring they can consistently deliver accurate and timely sustainability data.

The Investment Paradigm

There is no doubt that investor priorities are shifting– rapidly changing environmental and regulatory landscapes have pushed sustainability issues to centre stage for financial institutions. With the ISSB standards fostering a closer connection between sustainability practices and financial outcomes, companies which get this right can expect enhanced investor confidence. Conversely, those lagging behind may find themselves under greater scrutiny and potential divestment.

Operational and Strategic Adjustments

The ISSB standards, emphasising investor-centric financial materiality, signal a profound shift for company strategies and operations, especially for those in high carbon sectors, for example energy, heavy manufacturing and transportation. While the immediate impact of these standards may be more pronounced for industries with significant carbon footprints due to heightened scrutiny, the broader catalyst for change lies in evolving stakeholder expectations. As the market reacts to these reports, companies may need to adjust both strategy and operations to meet new demands and maintain competitiveness. Importantly, the ISSB standards can also serve as an advantage by providing companies with more detailed insights into carbon intensity, thereby facilitating better-informed decisions and fostering greater operational efficiency.

Bottom line

The new ISSB standards entail work! Intricate details can seem daunting, and initial investment in transforming practices will be significant. Demands for increased transparency and more robust reporting standards were inevitable - and there’s no escaping the changes required to our business models in order to meet evolving stakeholder demands. However, we see this as short-term pain for long-term gain. Dedicating resources towards getting reporting right will yield enhanced stakeholder trust, improved investor relations, and strategic resilience. Companies who are laser-focused on these outcomes are in the business of future-proofing and on the path to true sustainability.

External links:

ISSB issues inaugural global sustainability disclosure standards

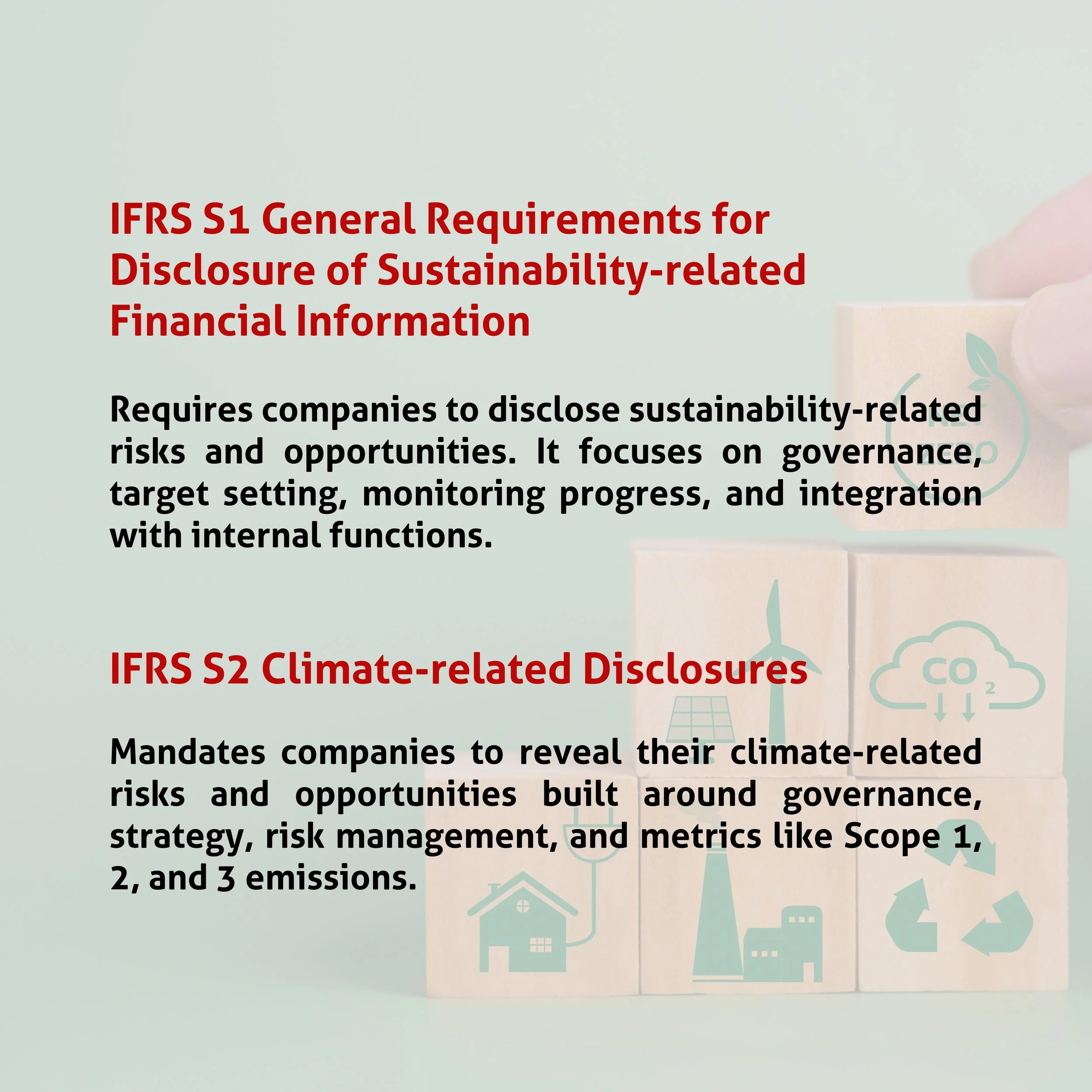

IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information

IFRS S2 Climate-related Disclosures

Related thinking